Table of Contents

The Q1 2026 deadline for ILPA v2.0 has passed. For funds still in their investment period, the updated ILPA Reporting Template is now the expected standard. Most GPs are aware of it. Far fewer are ready for what it means in practice, not just at reporting time, but during fundraising.

Most fund managers know LP expectations have risen. Fewer have caught up with where they now sit. Reporting quality is no longer benchmarked against last quarter’s pack. It is benchmarked against what institutional LPs consider the current standard, and that standard is ILPA v2.0.

For GPs actively fundraising or approaching a re-up cycle, this is the distinction that matters: ILPA v2.0 compliance is no longer a back-office concern. It is a competitive signal.

ILPA released the Reporting Template v2.0 in January 2025 as the core output of its Quarterly Reporting Standards Initiative (QRSI). It replaces the 2016 template for funds still in their investment period as of Q1 2026, and for all new funds commencing operations on or after 1 January 2026.

The changes are substantive. The 2016 template addressed fees and carried interest at a summary level. The 2025 version demands granularity across three areas:

The full guidance document is available at ilpa.org.

The shift is not regulatory. No rule currently requires ILPA v2.0 adoption. The pressure is coming from LPs directly, and it is showing up in due diligence.

Institutional LPs, particularly endowments, pension funds, and funds-of-funds, had already recalibrated their due diligence frameworks. The legal mandate disappeared; the investor mandate did not. ILPA v2.0 became the industry’s voluntary answer to the same transparency gap the SEC rules had tried to address.

The ILPA QRSI consultation process drew over 100 participating organisations across LPs, GPs, and service providers. That level of engagement does not happen around a standard investor’s plan to ignore.

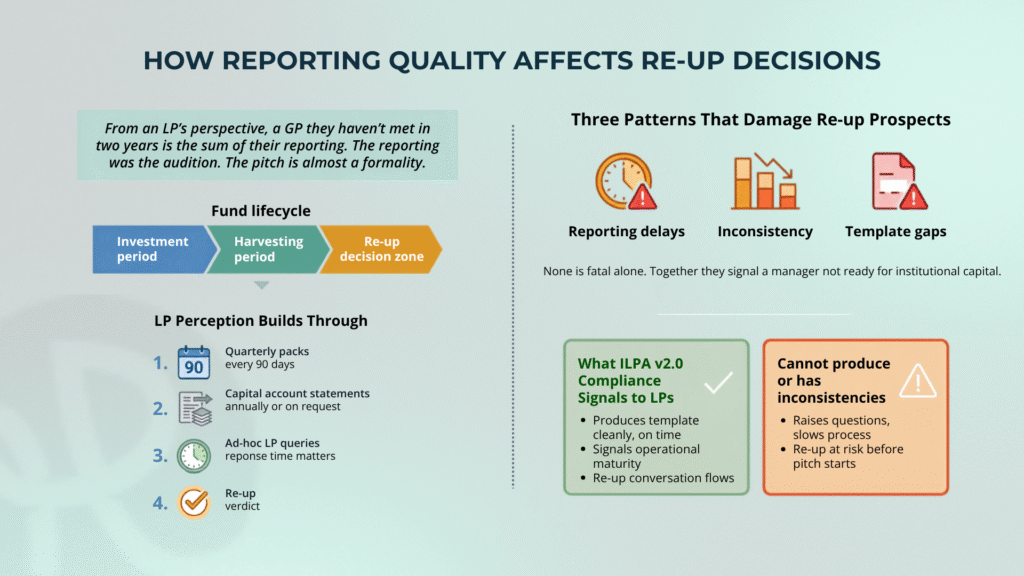

LPs conducting due diligence on a new commitment or a re-up are now comparing managers’ reporting practices against ILPA v2.0 as a reference point. A fund that cannot produce the template, or produces it with inconsistencies, raises questions that slow the process. A fund that produces it cleanly, on time, signals operational maturity.

From an LP’s perspective, a GP they have not met in person for two years is the sum of their reporting. Quarterly packs, capital account statements, and how quickly ad-hoc queries get answered: these are the touchpoints that shape the re-up decision, and they carry more weight than any pitch deck.

Three patterns consistently appear in funds that struggle with re-ups from institutional LPs:

None of these is fatal individually. Together, they create the impression of a manager who is not ready for institutional capital at scale. This is precisely the opposite signal a GP wants to send during a fundraise.

Fund CFOs and controllers typically understand the template requirements. What stops them is the data itself, sitting in disconnected systems, the fund administrator’s ledger in one place, internal chargebacks in a spreadsheet, portfolio company metrics somewhere else entirely.

The internal chargeback problem illustrates this clearly. Many GPs track the allocation of back-office costs across the fund, the management company, and portfolio companies in a spreadsheet maintained by the CFO or Controller. However, that spreadsheet is not connected to the fund administrator’s system. Under the 2016 template, the line items were flexible enough to accommodate the inconsistency. Under v2.0, the reconciliation has to be clean at each defined category.

For most GPs, ILPA v2.0 readiness requires three things to be in place:

Read more: What is IRR and how is IRR calculated?

For GPs working towards ILPA v2.0 compliance, the core operational problem is the disconnect between data held in portfolio companies, fund administrators, and internal finance teams. Therefore, when the investment team has to manually assemble data each quarter, errors accumulate, and deadlines slip.

Tools like Rundit offer an LP reporting template that centralises portfolio company data, including financial KPIs and operational metrics, so it flows directly into fund-level reporting without manual re-entry. Fund managers can prepare LP reports within the platform, structured to align with ILPA template requirements, and shared securely with LPs through a dedicated portal. The audit trail is preserved. Metrics stay consistent between periods.

For fund managers preparing for a fundraise or managing a re-up cycle, that consistency is the signal that matters to institutional LPs.

Read more: A Complete Guide to In-House LP Reporting for VC Firms

ILPA v2.0 is live. LPs are benchmarking GPs against it, whether or not the GP has formally adopted it. For funds still operating on manual processes or the 2016 template, the practical risk is not just a compliance gap. It is a fundraising gap.

GPs who build the infrastructure now, before the next reporting cycle, before the next LP meeting, before the next DDQ, will find the conversation with institutional LPs materially easier. Those who treat it as a future problem will find it has already become a present one.

Book a discovery call to see how Rundit supports ILPA-aligned LP reporting.