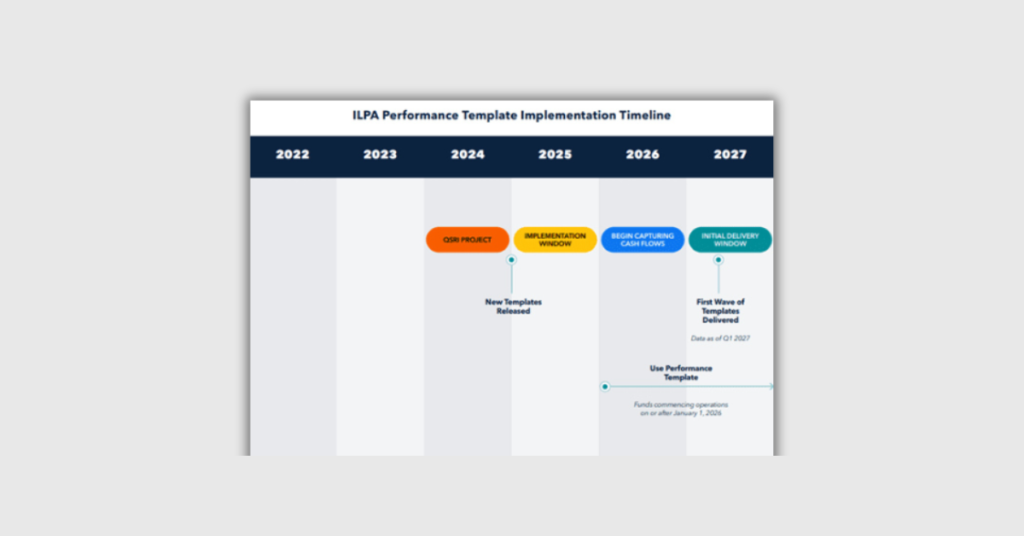

The new reporting template replaces the 2016 version and will be implemented on a go-forward basis for funds still in their investment period in Q1 2026, as well as for funds commencing operations on or after January 1, 2026.

According to ILPA’s new release, the new templates will be implemented beginning Q1 of 2026. Notably, these new guidelines do not apply to legacy funds whose investment periods end before the start of 2026.

This article will explore the key features of the updated ILPA Reporting Template and ILPA Performance Template, and what fund managers need to prepare for accounting systems to map accordingly with the implementation timeline in mind.

1. Key Updates to the ILPA Reporting Template

1.1 Expanded Partnership Expense Reporting

The 2025 ILPA Reporting Template significantly expands the scope of partnership expense reporting, increasing the number of required expense categories from nine to twenty-two. This comprehensive approach aims to provide Limited Partners (LPs) with a more granular and transparent view of fund operations.

Key additions to the expense categories include:

Offering and syndication costs: These encompass expenses related to fund formation and capital raising activities.

Placement fees: Costs associated with engaging placement agents or intermediaries for fundraising are now explicitly reported.

Partner transfers: Expenses incurred during the transfer of partnership interests between LPs are now tracked separately.

Third-party expenses: This category covers a wide range of external service providers, offering insight into the fund’s operational ecosystem.

Subscription facilities fees and interest: With the increasing use of subscription line financing, these costs are now reported distinctly.

Insurance fees: Fund-level insurance costs are now itemized, providing transparency on risk management expenses.

1.2 Enhanced Fee Transparency

The updated guidelines place a strong emphasis on fee transparency, addressing a long-standing concern in the industry, particularly for smaller LPs who often bear a disproportionate fee burden. The enhancements in this area are multifaceted:

Portfolio company fee reporting: GPs are now required to provide a more detailed breakdown of fees charged to portfolio companies. This includes management fees, monitoring fees, and any other charges that might impact the overall returns to LPs.

Expense reclassification disclosure: The guidelines mandate clear reporting on expenses that were previously covered by management fees but are now being charged as separate partnership expenses. This shift in expense allocation must be clearly communicated and justified.

Internal vs. external expense distinction: The new template requires GPs to clearly differentiate between expenses incurred by internal staff and those charged by external service providers. This distinction helps LPs understand the true cost structure of the fund’s operations and identify potential conflicts of interest.

Standardized fee reporting format: The guidelines introduce a more standardized format for reporting fees, making it easier for LPs to compare fee structures across different funds and managers.

1.3 Feeder Fund Reporting

Key aspects of the feeder fund reporting requirements include:

Direct fee and expense reporting: Feeder funds must now provide a detailed account of all fees and expenses incurred at the feeder fund level. This includes administrative costs, legal fees, and any other expenses specific to the feeder structure.

Master fund allocation transparency: The guidelines require feeder funds to clearly report their allocation of the master fund’s fees and expenses. This reporting must use the same line-item descriptions as the master fund, ensuring consistency and comparability.

Pro-rata expense allocation: Feeder funds must demonstrate how master fund expenses are allocated on a pro-rata basis to investors in the feeder structure, providing clarity on the true cost of investment through the feeder.

Performance reporting alignment: The performance metrics reported by the feeder fund must align with those of the master fund, with any discrepancies due to feeder-specific costs clearly explained.

Waterfall calculations: For feeder funds with carried interest calculations, the guidelines require transparent reporting on how these calculations are performed and how they relate to the master fund’s waterfall.

The new performance submission requires GPs to provide:

Net Internal Rate of Return (Net IRR): This metric shows returns after deducting fees and expenses, reflecting the true returns for Limited Partners (LPs). It’s crucial for evaluating overall fund performance, especially during fundraising.

Total Value to Paid-In capital (TVPI): TVPI provides a comprehensive view of fund performance by combining distributed and unrealized value.

A significant update in the new Performance Template is the requirement to report performance metrics both with and without the impact of fund-level subscription lines. Key aspects include:

Alignment with best practices: This update aligns with ILPA’s previous guidance on subscription line disclosure, which recommended quarterly disclosure of net IRR both with and without reliance on subscription line facilities

Dual reporting: GPs must now provide IRRs and TVPI/MOIC figures with and without the impact of fund-level subscription facilities.

Transparency: This approach aims to give LPs a clearer picture of the fund’s true performance, addressing concerns about the potential distortion of reported fund performance figures due to subscription line usage.

Applicable to: Actively investing funds as of January 1, 2026

Legacy Funds: Funds with investment periods ending before the start of 2026 are not required to adopt the new guidelines

Image from https://ilpa.org/

4. Industry Impact

4.1 Increased Transparency and Standardization

The new guidelines aim to provide LPs with:

Better insight into the direct costs of fund participation

A comprehensive schedule of fees and reimbursements received by investment advisors or related persons

Improved ability to compare funds and assess true costs

4.2 Addressing Industry Trends

These updates respond to several industry trends:

Evolving practices in private equity fund economics

Changes in GP disclosures

The expanding role of service providers in the alternatives industry

4.3 Meeting Investor Needs

With allocations to alternative asset classes rising (from 23% in 2013 to 34% in 2024 among top US pension funds), investors require more detailed information to:

Assess risks

Justify costs to stakeholders

Make informed allocation decisions

5. ILPA Reporting Excellence: Actionable Strategies for GPs and LPs

For General Partners (GPs)

For Limited Partners (LPs)

→ Review and update internal accounting systems to accommodate new reporting requirements.

→ Develop processes for more granular expense tracking.

→ Prepare for increased transparency in portfolio company fee arrangements.

→ Consider the impact on resource allocation for reporting and compliance.

→ Familiarize yourself with the new reporting format and expanded expense categories.

→Develop analytical tools to leverage the additional data effectively.

→ Engage with GPs to understand their implementation plans and timelines.

→ Consider how the new information will impact investment decision-making processes.

6. Conclusion

The ILPA 2025 Reporting Guidelines represent a significant step towards greater transparency and standardization in private equity reporting. By providing more granular detail on partnership expenses and standardizing performance metrics, these guidelines aim to foster better alignment between GPs and LPs. As the industry continues to evolve, staying informed and prepared for these changes will be crucial for all participants in the private equity ecosystem.

Disclaimer: The information provided above is for general informational purposes only and does not constitute investment advice. Every investment situation is unique, and these guidelines may impact different investors in various ways. We strongly recommend consulting with qualified financial advisors or legal professionals to understand how these changes specifically affect your investment strategy or reporting obligations. For the most up-to-date and detailed information, please refer to the official ILPA website.

Looking to Automate the Reporting Process?

Rundit offers a solution that not only simplifies compliance with ILPA reporting standards but also enhances the overall investor experience. Our platform streamlines the process of generating insightful reports, allowing fund managers to present data in a clear and engaging manner. With features designed to accommodate both ILPA and global LP expectations, Rundit helps you maintain transparency while saving valuable time.

Schedule a demotoday and see firsthand how our platform can transform your approach to investor reporting and engagement!