Venture capital (VC) is a high-stakes game where investors aim to identify and back startups with the potential for exponential growth. However, it’s not just about intuition and gut feeling; there is a significant amount of mathematics and financial modelling involved in making these investment decisions. Understanding the core principles of “Venture Capital Math” (VC Math) can help both founders and investors navigate this complex landscape.

Venture capitalists raise money from limited partners (LPs) such as pension funds, endowments, and high-net-worth individuals, and then invest this money into a portfolio of startups. In return, they take equity in these startups, hoping that a few will yield substantial returns that will outweigh the losses from the many that fail.

To succeed, VCs rely on specific mathematical frameworks and key financial metrics to evaluate potential investments and manage their portfolios effectively. Let’s dive into the numbers that drive these decisions.

Here are some of the essential metrics used in venture capital math:

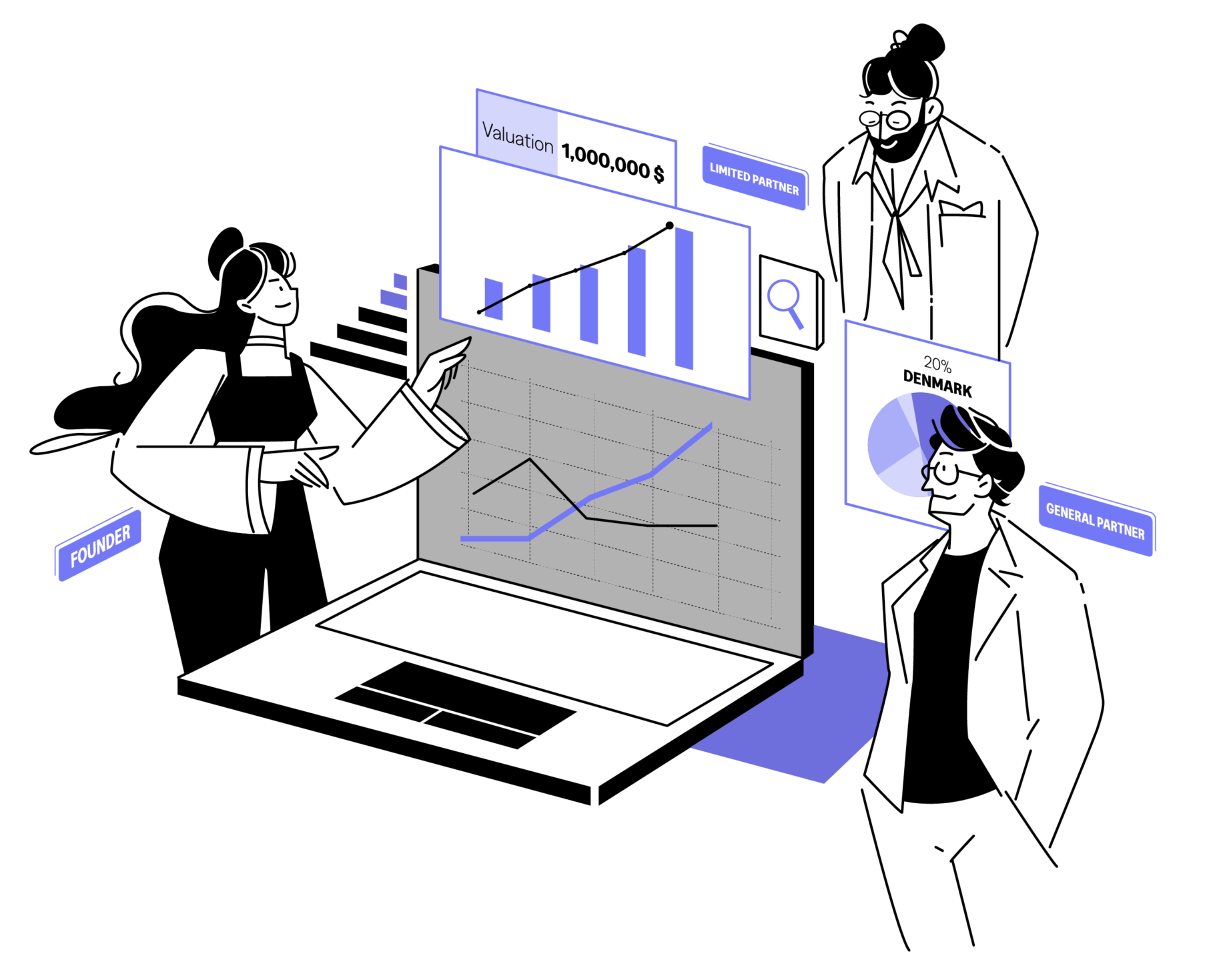

The ownership percentage is the share of the company a VC gets in exchange for their investment. This is determined by the valuation of the company before the investment (pre-money valuation) and the amount being invested.

Ownership Percentage = Investment Amount / (Pre-Money Valuation + Investment Amount)

For example, if a VC invests 5 million in a startup with a pre-money valuation of 20 million, the ownership percentage would be:

Ownership Percentage} = 5 / (20 + 5) = 20%

The post-money valuation is the value of the company after the VC investment has been made.

Post-Money Valuation = Pre-Money Valuation + Investment Amount

Using the previous example:

Post-Money Valuation = 20 + 5 = 25 million

Dilution refers to the reduction in ownership percentage of existing shareholders when new shares are issued. For startups, dilution is a natural consequence of raising new rounds of funding.

To calculate the dilution impact:

New Ownership Percentage = (Old Ownership Percentage × Pre-Money Valuation) / Post-Money Valuation

Venture capitalists invest in startups with the expectation of high returns. The ROI is calculated to determine the profitability of an investment.

ROI= (Exit Value−Investment Amount ) / Investment Amount

The IRR is the annualized rate of return expected from an investment over a specific period. It’s a more complex metric that takes into account the time value of money and the timing of cash flows. It’s a key metric used by VCs to compare different investments.

Venture capital is heavily influenced by the “Power Law,” which states that a small number of investments will generate the majority of the returns. In a typical VC portfolio, a few companies may provide outsized returns, while the majority may fail or only break even.

VCs aim to construct a portfolio where at least one or two investments can provide a 10x to 100x return to make up for the losses or smaller returns from other companies. To achieve this, they use mathematical models to allocate capital across a range of startups, balancing the risk and reward.

Venture capitalists often use an expected value formula to gauge the potential outcomes of an investment.

Expected Value = (P 1 ×R 1 )+(P 2 ×R 2 )+…+(P n ×R n )

Where P is the probability of each outcome, and R is the return in each scenario. This helps them estimate the average return they might expect over time, despite the high failure rate of startups.

The ultimate goal of a VC investment is to achieve a successful “exit,” such as an Initial Public Offering (IPO) or acquisition, where they can sell their shares at a significant profit.

To assess potential exit scenarios, VCs often estimate the exit valuation of a company. They use various methods, including:

A waterfall analysis determines how proceeds from an exit will be distributed among investors, founders, and other stakeholders. This is crucial to understand potential returns and how different liquidation preferences, such as 1x or 2x liquidation multiples, will affect the distribution.

Venture capital firms are evaluated based on their ability to generate returns for their limited partners. The two primary metrics used are:

a) Multiple on Invested Capital (MOIC)

MOIC measures the total value returned to investors relative to the total amount invested.

b) Total Value to Paid-In Capital (TVPI)

TVPI is the ratio of the current value of the portfolio (both realized and unrealized) to the total capital invested. It’s used to assess the overall performance of the fund, including both realized exits and current portfolio companies.

While venture capital may seem like a world driven by instinct and relationships, it is underpinned by mathematical analysis and financial modelling. By understanding the key metrics and frameworks that drive VC decision-making, both founders and investors can better navigate the complexities of the startup ecosystem. Whether you are a founder seeking funding or an aspiring venture capitalist, mastering these mathematical concepts is crucial to success in the world of venture capital.

Rundit offers a powerful solution tailored for venture capital firms, helping them manage and analyze these critical metrics with ease. Our platform provides comprehensive dashboards, advanced data visualization, and centralized data management, enabling your team to make data-driven decisions that align with your investment strategies. Don’t let the complexities of venture capital math overwhelm you—contact us today to discover how Rundit can help your firm optimize its investment process and achieve superior returns.

Additional resources:

Understanding Venture Math 🔗 – Pitching Angels

What is IRR and how is IRR calculated? 🔗 – Rundit

Consolidate your portfolio and fund data in one single platform. One source of truth for your team’s investment data.